The Cardi B Problem

On February 9, 2026, during Bad Bunny's Super Bowl LX halftime show, Cardi B walked out onto the stage. She danced on the porch of “La Casita” alongside Karol G, Young Miko, and Pedro Pascal. She moved to the music. She did not hold a microphone.

What happened next was a $57 million question.

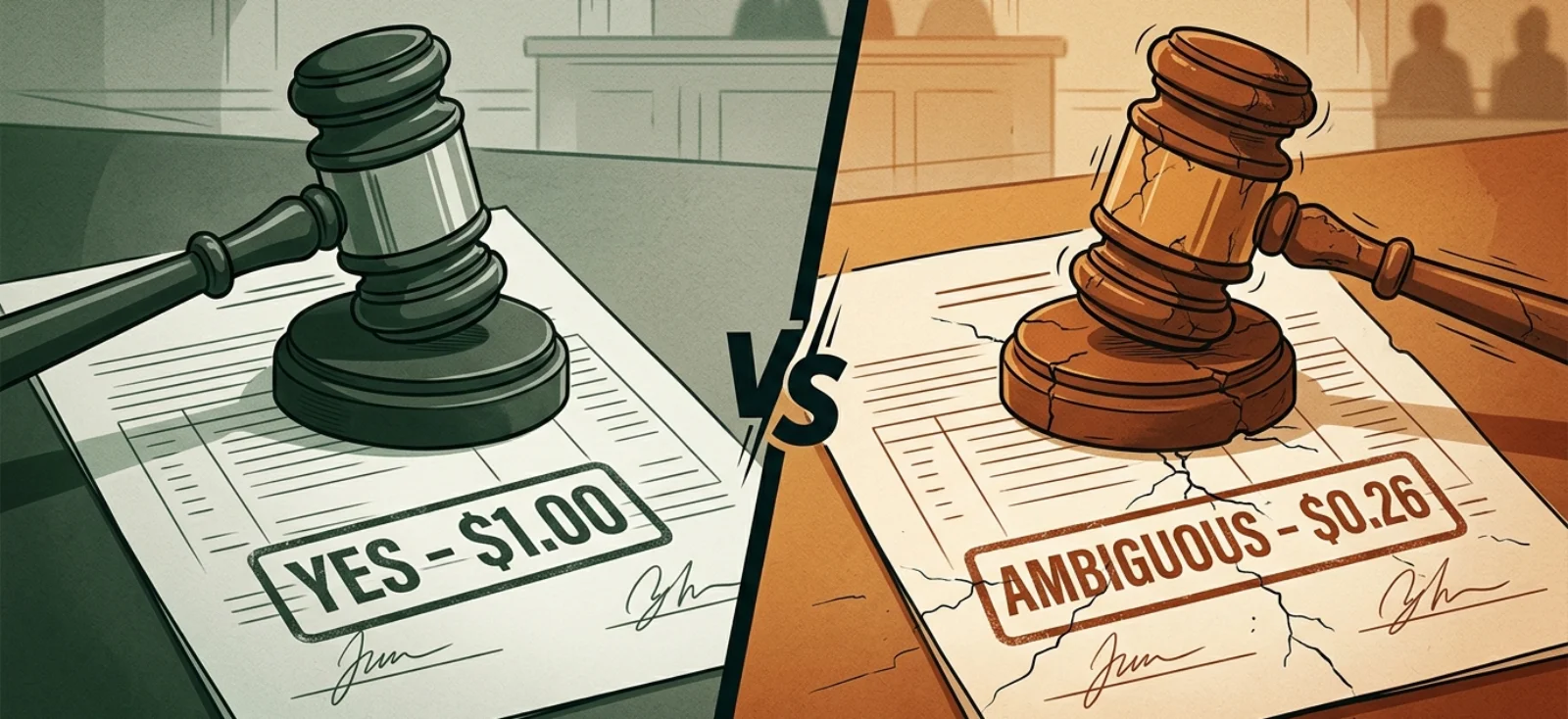

Cardi B Super Bowl Halftime — YES contract payout

Same event. Same footage. Different contracts.

Did Cardi B perform at the Super Bowl?

Resolved YES at $1.00. "Participation in the halftime show without singing" counted as a qualifying performance. Media consensus: she performed.

YES → Paid $1.00Invoked Rule 6.3(c). "Ambiguous" — singing and dancing counted, but "just dancing in the background" did not. Settled at last traded price.

AMBIGUOUS → Paid $0.26Same footage. Same performance. $47.3 million in Kalshi volume. $10 million on Polymarket. If you'd tried to “arbitrage” the price gap between platforms by buying YES on one and NO on the other, you would have lost money on both sides.

A Kalshi trader filed a CFTC complaint seeking $3,700 in restitution. The contract was clear, the trader argued — she performed. Kalshi's response: the contract was clear too — “dancing in the background” doesn't count.

Why “risk-free” arbitrage isn't

Spot a “price gap”

“Cardi B performs?” — YES at 74% on Kalshi, 85% on Polymarket

Execute the “arb”

Buy YES on Kalshi (cheap), buy NO on Polymarket (cheap). Guaranteed $1 payout from one side... right?

The event happens

Cardi B dances on stage. Did she “perform”? Depends who you ask.

The trap

Polymarket resolves YES → your NO loses. Kalshi invokes “ambiguous” → your YES gets $0.26, not $1.00. You lose on both sides.

This is what settlement risk looks like. Not a black swan. Not a hack. Just two platforms reading the same event and reaching different conclusions, because they wrote different rules.

The $54 Million Death Carveout

On February 28, 2026, U.S.-Israeli military strikes killed Iran's Supreme Leader Ali Khamenei. Across prediction markets, contracts asking whether Khamenei would “leave office” should have been straightforward.

On Polymarket, the equivalent market accumulated over $529 million in volume. It entered UMA's dispute process and eventually resolved as expected.

On Kalshi, things went differently. The market — titled “Ali Khamenei out as Supreme Leader?” with user-facing rules stating “If Ali Khamenei leaves office before March 1, 2026, then the market resolves to yes” — had accumulated $54 million in trades. But Kalshi invoked what became known as the “death carveout.”

The death carveout

Buried in Kalshi's filed CFTC contract terms was language specifying that if the subject of a contract dies, the market settles at the “last traded price prior to confirmed reporting of death” rather than resolving YES or NO. This language was not prominently displayed on the market page. Kalshi later acknowledged their disclosures were “grammatically ambiguous.”

YES holders on Kalshi received fractional payouts instead of the full dollar. The class action lawsuit (Risch v. KalshiEX LLC) argued that “with an American naval armada amassed on Iran's doorstep, consumers understood that the most likely — and in many cases the only realistic — mechanism by which an 85-year-old autocratic leader would 'leave office' was through his death.”

Kalshi CEO Tarek Mansour defended the carveout as preventing “profiting from death.” The company reimbursed all fees and net losses — reportedly around $2.2 million — so no customer ended net-negative. On March 2, Kalshi filed a formal rulebook amendment with the CFTC codifying Rule 6.3(e): a universal death settlement rule for all future contracts.

Meanwhile, a trader using the handle “Magamyman” made $553,000 on Polymarket's equivalent market, which resolved normally. Israeli authorities separately charged two individuals for using classified intelligence to place bets.

Two platforms. Same dictator. Same death. Wildly different outcomes for traders.

When the Oracle Lies: The $7M Governance Attack

If Kalshi's problem is centralized power — one company writing and interpreting its own rules — Polymarket's problem is the opposite: decentralized resolution that can be bought.

In March 2025, a market asking whether Ukraine would agree to a mineral deal with Trump before April accumulated over $7 million in volume. No deal was signed. The market should have resolved NO.

Instead, a UMA token whale used 5 million UMA tokens across three accounts — representing roughly 25% of total voting power — to force the market to resolve YES. The attack exploited a structural vulnerability: UMA's circulating market cap (~$44M) was a fraction of Polymarket's total value locked (~$330M). It was cheaper to buy enough tokens to control the oracle than the capital at risk in the market.

Polymarket acknowledged the outcome was wrong but called it “unprecedented” and offered no refunds.

This wasn't the only incident. The $237M Zelenskyy suit market — asking whether the Ukrainian president would wear a suit before July 2025 — entered a 9-day dispute cycle after he appeared at NATO in a black jacket and matching trousers. UMA voters eventually ruled NO (not a suit), flipping YES shares from $0.19 to $0.04. The top 10 voters controlled roughly 30% of the vote. Critics pointed out that UMA's $95M market cap was governing a $242M market.

Compare contract terms on PredictMarketCap

Timeline: When settlement went wrong

UMA whale forces false YES with 5M tokens. $7M market. No refunds.

$237M market. 9-day UMA dispute. YES flips to NO. Top 10 voters control 30%.

Polymarket adds Chainlink for price markets. Partial fix for oracle risk.

Kalshi: ambiguous ($0.26). Polymarket: YES ($1.00). Same footage. $57M total.

$54M market. Undisclosed death rule. Class action filed. Rule 6.3(e) created.

Three Ways to Decide What Happened

Every prediction market platform has to answer the same question: when the event happens, who decides the outcome? The three major models each have distinct failure modes.

How the same event flows through different systems

Kalshi

CFTC-regulated. Internal markets team determines outcomes using named Source Agencies (AP, NOAA, BLS, Federal Reserve).

Cardi B: $47M settled as "ambiguous." Khamenei: death carveout not clearly disclosed.

Polymarket

UMA Optimistic Oracle. Proposer stakes $750 bond, 2-hour challenge window, disputes escalate to UMA token-holder vote.

Ukraine mineral deal: whale spent $5M in UMA tokens to force false YES resolution on $7M market.

Limitless

Dual model: Pyth Network oracles for price data, internal team for subjective markets. Refund policy for misresolutions.

Newer platform with less resolution history. Tradeoff: speed and simplicity over battle-tested dispute processes.

The uncomfortable truth: there is no resolution mechanism that has proven itself reliable at scale. Centralized models have the Kalshi problem (unilateral power, undisclosed rules). Decentralized models have the Polymarket problem (capital-weighted voting, oracle manipulation). Hybrid models are unproven.

The Price Gaps Are Real — and They're Not Arbitrage

We track cross-platform markets across Polymarket and Kalshi. When prices diverge, the instinct is to call it arbitrage. But dig into the contract terms and a different picture emerges.

Live cross-platform price gaps (as of March 25, 2026)

The James Bond gap is instructive. It looks like a 28.5 percentage-point arbitrage opportunity. But Polymarket is asking “will Callum Turner be announced as the next James Bond by June 30, 2026?” while Kalshi is asking the same question with a deadline of January 1, 2030. Those extra 3.5 years of optionality are worth a lot. The price difference isn't a market inefficiency — it's two different bets.

The CA-11 primary gap is even subtler. Both platforms are asking about the same election on the same day. But California's jungle primary advances the top two finishers to the general election. Kalshi resolves on “who advances” (two winners possible), while Polymarket resolves on “who gets the most votes” (one winner). The contract structures aren't compatible.

One pattern stands out: Kalshi consistently prices higher across genuine matches. Rubio, Newsom, Russell, Sabres, Spain, Lula — all higher on Kalshi by 2–5 percentage points. This could reflect different user demographics, Kalshi's lower liquidity allowing prices to drift, or the regulatory premium of trading on a CFTC-regulated exchange.

The Academic View: “Semantic Non-Fungibility”

Researchers Jonas Gebele and Florian Matthes put a name to this problem in their January 2026 paper: “Semantic Non-Fungibility and Violations of the Law of One Price in Prediction Markets.”

Key finding: Across 100,000+ events on 10 platforms, semantically equivalent markets show persistent 2–4% median price deviations. Only ~6% of events are listed on multiple platforms. Arbitrage is structurally difficult: positions cannot be netted across venues and must be held to resolution.

The core insight: prediction markets lack a shared, machine-verifiable notion of event identity. Unlike stocks (which have CUSIP/ISIN identifiers) or options (with standardized contract specs), prediction market contracts are defined by platform-specific natural language, resolution rules, oracle sources, and cutoff times. Whether two markets actually promise the same payoff is a legal question, not a mathematical one.

The paper provides a concrete example we can verify with our own data: the 2024 U.S. Presidential Election. Polymarket resolved when AP, Fox News, and NBC all called the race — the morning after Election Day. Kalshi resolved on inauguration, January 20, 2025. Same question. Same winner. But your capital was locked for 75 extra days on Kalshi.

2024 Presidential Election: same winner, different settlement

Resolved Nov 6 (morning after). AP + Fox + NBC all called it.

Capital locked: ~12 hours

Resolved Jan 20 (inauguration). Most objective possible trigger.

Capital locked: ~75 days

Even weather markets diverge. Kalshi uses the NWS Central Park station for NYC temperature markets. Polymarket uses LaGuardia Airport via Weather Underground. The stations are 8 miles apart and can record temperatures 1–3°F apart on any given day — enough to push the reading into a different resolution bucket.

NYC temperature markets: same city, different thermometers

8 miles apart. 1–3°F difference. Different resolution bucket.

What Needs to Change

Listed derivatives solved this problem decades ago. If you buy an S&P 500 option, the contract specs tell you exactly what triggers settlement, how it's calculated, and when it's final. You can hedge a position in SPY options with an offsetting position elsewhere because the contracts are fungible. That's what makes liquid markets work.

Prediction markets are nowhere close to this. And the industry knows it. Solidus Labs has flagged “the absence of standardized symbology” as one of six structural surveillance gaps. The Gebele/Matthes paper calls resolving event identity “a prerequisite for prediction markets to aggregate information at a global scale.”

Some progress is happening. Polymarket partnered with Chainlink in September 2025 to automate price-based market resolution, reducing UMA's role. Kalshi codified Rule 6.3(e) after the Khamenei controversy, bringing more transparency to edge cases. Polymarket upgraded to a Managed Optimistic Oracle (MOOV2) with 37 whitelisted proposers after the Ukraine attack.

But no one is working on cross-platform standardization. There's no equivalent of CUSIP for prediction markets. No shared resolution framework. No interoperability standard that would let a trader offset a position on one platform with a hedge on another.

Until that changes, every cross-platform comparison comes with an asterisk. Including ours.

What we're doing about it

PredictMarketCap now shows side-by-side contract comparisons on every cross-platform event page, with word-level highlighting of differences and similarity scores. Our arbitrage scanner includes settlement risk warnings. These are imperfect tools — they can't tell you how an ambiguous event will be resolved — but they surface the contract differences that matter most.

How to Protect Yourself

If you trade on prediction markets, especially across platforms:

- Read the resolution rules, not just the question. The question is marketing. The rules are the contract. “Will X happen?” can mean ten different things depending on how “happen” is defined.

- Check the resolution source. Who decides the outcome — AP? NOAA? A DAO vote? An internal team? This is the single most important piece of information in any contract.

- Check the resolution timeline. A market that resolves on election night and one that resolves on inauguration are different bets. A market expiring in 2026 and one expiring in 2030 are very different bets.

- Understand the edge cases. What happens if the event is “ambiguous”? What happens if the subject dies? What happens if the data source goes offline? The boring edge cases are where money gets lost.

- Price spreads are not always arbitrage. A 5% gap between platforms might reflect a genuine pricing inefficiency. Or it might reflect a contract term difference that makes the positions non-fungible. Before committing capital to “risk-free” arbitrage, confirm the contracts are actually equivalent.

Know someone trading across platforms? They should read this.

PredictMarketCap tracks contract differences across Polymarket, Kalshi, and Limitless in real time.

Methodology & Sources

Price data reflects prediction market odds tracked by PredictMarketCap as of March 25, 2026. Cross-platform price gaps are computed from our canonical event matching system, which uses AI-assisted comparison of market questions and outcomes. Contract term differences are sourced from each platform's published rules.

Case study sources: Cardi B dispute ( Fortune, Front Office Sports), Khamenei death carveout ( Wired, ClassAction.org), UMA governance attack ( The Defiant), academic research ( Gebele & Matthes 2026).

PredictMarketCap is an independent data aggregator. We are not affiliated with any prediction market platform. This analysis is not financial advice.

FAQ

What is settlement risk in prediction markets?

Settlement risk is the chance that two markets tracking the same event resolve differently because they use different rules, data sources, or resolution authorities. A "risk-free" arbitrage becomes a loss if one platform pays out and the other doesn't.

Is cross-platform prediction market arbitrage safe?

Not necessarily. While price differences between platforms can represent genuine arbitrage opportunities, they often reflect different contract terms, resolution criteria, or settlement timelines. Always read the full contract rules on both platforms before trading.

How does Polymarket resolve markets?

Polymarket primarily uses the UMA Optimistic Oracle, where token holders vote on outcomes. A proposer stakes a bond, there's a challenge window, and disputed markets escalate to UMA token-holder vote. This is decentralized but vulnerable to whale manipulation, as seen in the Ukraine mineral deal incident.

How does Kalshi resolve markets?

Kalshi is a CFTC-regulated Designated Contract Market. An internal markets team determines outcomes based on named "Source Agencies" (AP, NOAA, BLS, etc.) specified in each contract. Rule 6.3(c) allows settlement at last-traded price for "ambiguous" outcomes.

What happened with the Cardi B Super Bowl prediction market?

Kalshi ruled Cardi B's appearance "ambiguous" (she danced but didn't have a microphone) and settled at last-traded price — YES holders got $0.26. Polymarket resolved YES at $1.00 using media consensus. Same footage, opposite payouts.

Get the next analysis in your inbox

We write when the data says something interesting. No spam, unsubscribe anytime.